Aquestive Therapeutics (AQST): Underappreciated Late-Stage Assets Present Significant Long-Term Opportunity Despite Recent Gains

Sublingual form of EpiPen presents a paradigm shift for patients; potential to capture share and expand overall market size.

**NOTE: Smaller updates are on covered companies and positioning are posted to Twitter. For thoughts on the $75 million offering, see this post.**

Executive Summary

Aquestive Therapeutics AQST 0.00%↑ is a unique late-stage, multi-asset biotech company which has attracted attention in recent weeks for its sublingual formulation of epinephrine, Anaphylm, which is being developed for the treatment of severe allergic reaction and anaphylaxis. The company reported positive (largely expected) results from a pivotal Phase 3 trial on March 14th confirming that Analphylm contains a similar pharmacologic profile to that of EpiPen (Mylan), but with the enormous advantage of being needle-free and small enough to fit in the back of an iPhone case.

Anaphylm’s convenient form factor and route of administration could not only improve patient experience, but will also likely expand the epinephrine market, which is currently ~$1 billion, by unlocking the 50-60% of at-risk patients that either don’t fill their prescription or do not carry their epinephrine auto-injector because of needle anxiety or product bulkiness.

While there are a few companies developing nasal spray formulations of epinephrine, including ARS Pharma’s (SPRY) Neffy, Aquestive is the only company developing a sublingual version, which we think will ultimately capture leading market share because of its ability to be stored passively in the back of patients’ phone case or wallet, providing “always-on” protection and alleviating the hassle and memory burden of an additional personal item (i.e. the intranasal device case).

Beyond Anaphylm, Aquestive has a number of other attributes which make it a unique company and an interesting long-term investment:

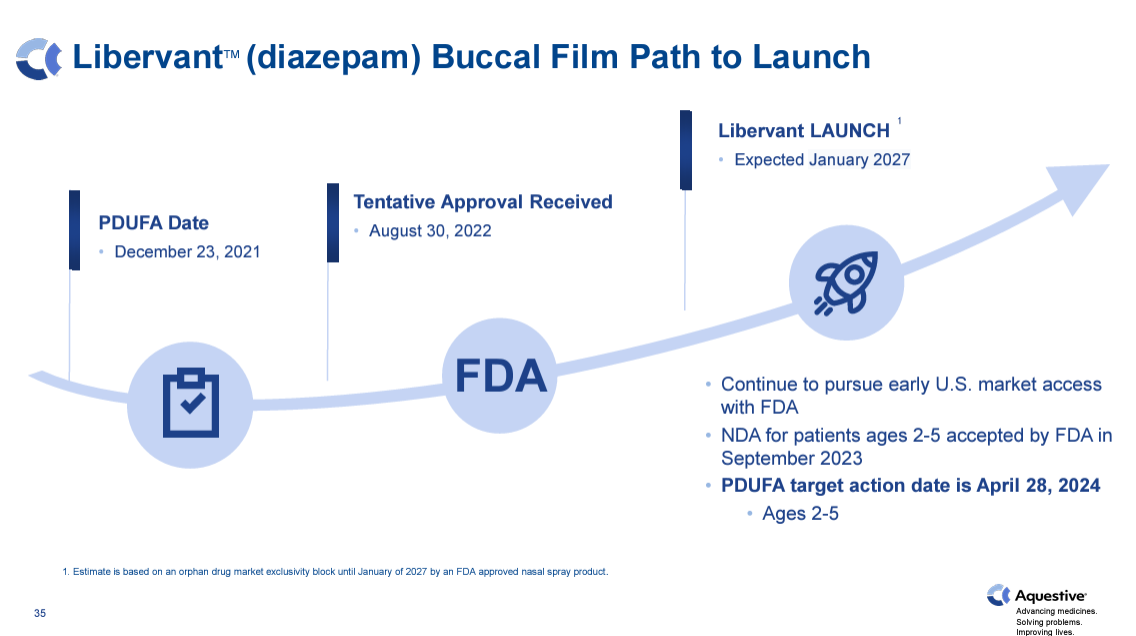

It is advancing Libervant, the only sublingual form of diazepam (i.e. Valium) for cluster seizures in children ages 2-5, with a PDUFA (FDA approval) decision due April 28th. The only other drug approved for this cohort is diazepam rectal gel. Libervant could begin generating preliminary revenue in the 2H24 and, upon label expansion, has a well-defined path to $100+ million of annual revenue.

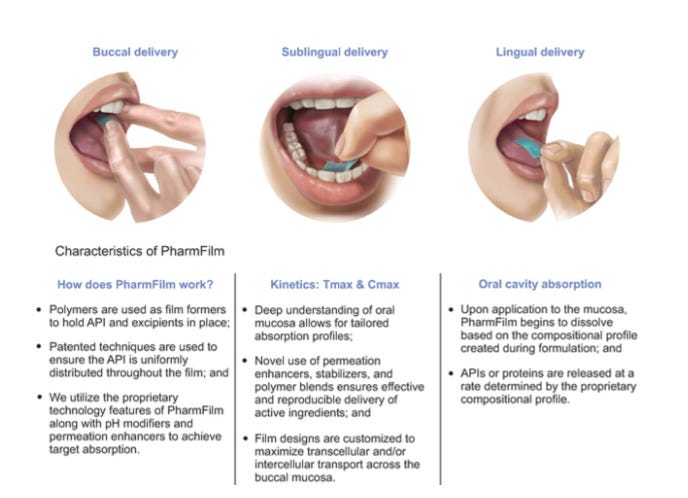

Developed PharmaFilm, the oral film technology that enables sublingual delivery of Anaphylm and Libervant. Is the world leader in oral film drug delivery as well as manufacturing, with capacity to manufacture more than one billion commercial doses per year. Holds 150 patents worldwide.

Has a licensing and drug manufacturing business of sublingual formulations of generic drug compounds (e.g. Suboxone, Exservan) which generated $50 million of sales in 2023. The base business is (marginally) profitable and has helped Aquestive to remain relatively self-sufficient over the past couple years, drawing just $9 million from its ATM facility during 2023 to keep cash relatively stable at $24 million.

Using its absorption/formulation technology and know-how, is developing a topical cream, AQST-108, which is currently in a first-in-human trial and for which the company expects to announce a lead dermatological indication later in 2024. We think the company may target atopic dermatitis (17+ million US patients).

Aquestive also touts its “Adrenoverse” platform, a library of epinephrine/adrenaline prodrugs, from which Anaphylm and AQST-108 were created.

While most of the dialogue surrounding Aquestive revolves around Anaphylm, Libervant is an interesting running mate. Libervant was actually granted “tentative approval” by the FDA in seizure patients aged 12+ (including adults) in August 2022, but is blocked from entering the market until January 2027 due to an Orphan Drug Exclusivity (ODE) that was awarded to Neurelis’ (private) Valtoco, an intranasal formulation of the same drug, diazepam, which was approved in 2020 in patients ages 6+. Valtoco did $115 million of revenue in 2023 (60% y/y growth), underscoring the longer-term opportunity.

In the meantime, we believe approval of Libervant in ages 2-5 in April is likely, and believe there is some potential for off-label use in older patients. The company states that it is in active discussions to partner Libervant with a CNS-focused partner. Aquestive also intends to out-license the ex-US rights to Anaphylm this year, while retaining US commercial rights in-house.

With two products that have clearly-defined value propositions expected to reach the market in 2024 and 2025, respectively, Aquestive presents a strong near- and medium-term growth story which also doubles as a foundation upon which the company can continue to add value via its AQST-108 topical cream, additional licensing deals for its PharmFilm technology, as well as other internally-developed products.

We have built a position in Aquestive over the past couple weeks and believe the current valuation is attractive even after a 16% gain on Friday which brought its market cap to $445 million. Significant further upside potential is supported both on a fundamental basis for Anaphylm, which we project reaching $700+ million of annual sales by 2028, as well as on a relative valuation basis versus ARS Pharma, which trades at an $880 million market cap despite having no drug pipeline outside of Neffy, suggesting 97% upside potential for Aquestive in the more immediate-term.

In all, we think Aquestive is an attractive opportunity to augment our biotech portfolio with a later-stage, relatively de-risked company with unique attributes and long-term growth potential.

Anaphylm

Based on our reading of available data, we believe Anaphylm’s pharmacokinetic (PK) and pharmacodynamic (PD) profile is equivalent or even superior to currently marketed options (i.e. manual injection, EpiPen, Auvi-Q), as well as the other “next-generation” intranasal epinephrine drugs.

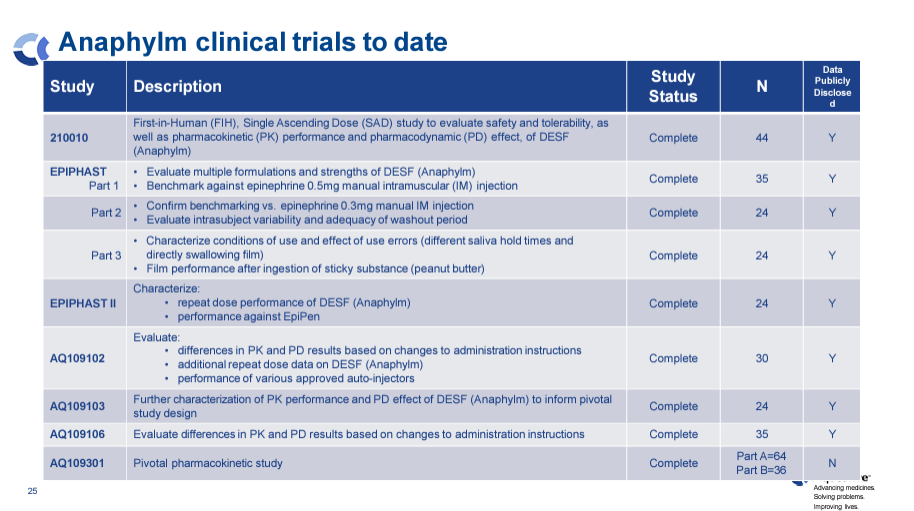

Including the recently-announced pivotal Phase 3 trial, Anaphylm has been trialed in 340 healthy volunteers across 7 clinical trials.

Trials to date show that Anaphylm:

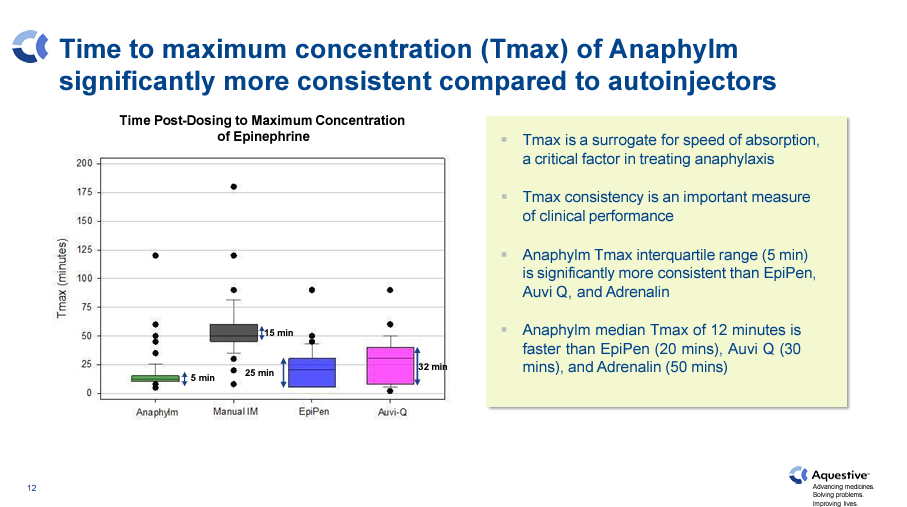

Reaches maximum concentration (Tmax) in about 12 minutes, quicker than that of auto-injectors (25-40 minutes) and Neffy (20-30 minutes). Speed of onset is a key factor in allergic reaction and anaphylaxis, and may be an additional differentiator for Anaphylm. Additionally, Anaphylm shows less variability in its Tmax versus injectables (i.e. is more predictable).

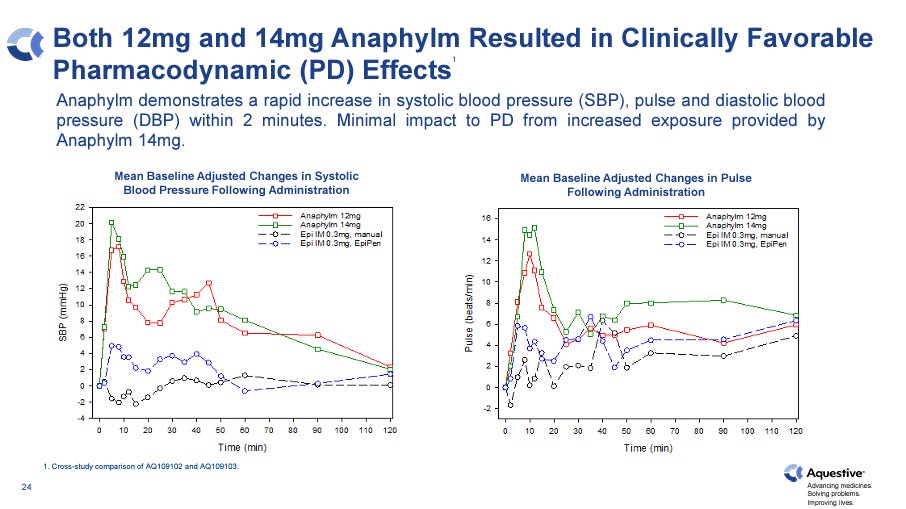

Causes systolic blood pressure (SBP) increases of up to ~16 mmHg within 5-10 minutes (for 12mg dose), which is indicative of epinephrine-induced vasoconstriction (i.e. on-target activity). This response is significantly greater than injectable products and comparable to two Neffy spray doses. Anaphylm’s SBP effect is also more rapid than Neffy’s.

Concentration of epinephrine in plasma stays above 100 pg/mL in the blood for more than 60 minutes. 100 pg/mL is considered the efficacy threshold concentration by the FDA.

Predictable responses upon re-dosing, which is required in some patients with more severe reactions or absorption irregularities. 100% of patients which failed to reach the 100 pg/mL after their first dose achieved within 20 minutes upon Anaphylm repeat dosing, versus 45 minutes for EpiPen.

Has a strong safety profile, comparable to or better than injectable products, and without the risk of injection complications such as accidental intravenous injection.

The company has also run trials which have addressed potential concerns with sublingual administration. Namely, Aquestive conducted:

A study in volunteers who had just eaten a peanut butter sandwich (a sticky food that coats the inside of the mouth), which showed no significant interference with drug absorption.

A study of patients that immediately swallowed the Anaphylm square whole. Tmax remained consistent at 12 minutes and Cmax remained comparable with proper sublingual administration.

Anaphylm has also been found to remain stable and active when exposed to rain and direct sunlight because of its primary packaging (the bandage wrapper-like package containing the oral film square).

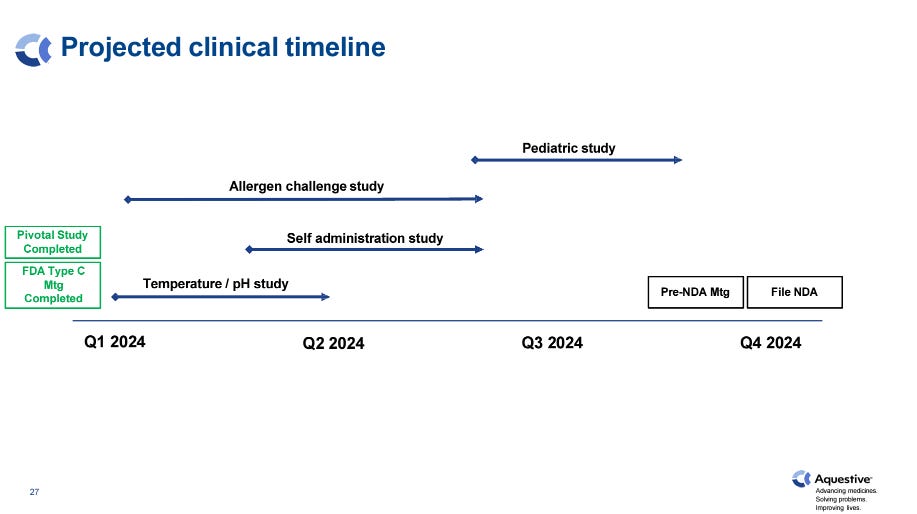

Following the pivotal Phase 3 study, Aquestive had a meeting with the FDA. Aquestive reports that it believes it is aligned with the FDA, and has just a few small characterization studies left to complete before it can submit an NDA for Anaphylm later this year:

These studies were already planned by Aquestive based on its end-of-Phase 2 meeting with the FDA in November 2022. Of note, Aquestive received guidance from the FDA that it could run its Allergen PK Study, which is a study of Anaphylm administration in patients experiencing an allergic swelling reaction of the lips/mouth/tongue, could be conducted as a challenge trial, which is significantly easier to run than the trial design the company was previously planning.

Given the nature of the indication, these studies are very quick and inexpensive to complete, and the company expects to engage in a pre-NDA meeting in the 3Q24 or 4Q24.

Intranasal vs. Sublingual

In addition to ARS Pharma, there are three other companies developing nasal spray products, namely Bryn Pharma (private), Orexo, and Amphastar Pharmaceuticals, all of which are aiming to file for approval in 2024 or 2025. Conversely, we are not aware of any other sublingual formulations competing with Anaphylm, which further speaks to Aquestive’s leadership in the sublingual formulation space. It is our contention that in the real-world setting, Anaphylm’s sublingual route of administration will prove to be far more convenient and practical for patients than intranasal, and thus Anaphylm will ultimately win the largest share of the market, likely larger than the multiple intranasal devices combined.

While intranasal administration, like sublingual, solves the needle hesitancy issue, there is still the convenience/bulkiness issue. While the Neffy case is better than an EpiPen, at-risk patients do not want to carry around yet another item the size of a wallet which they have to keep track of, remember to carry, etc. While it is a simple concept, we believe Anaphylm’s ability to “set it and forget it” in the back of a phone case or wallet is a complete paradigm shift for at-risk patients.

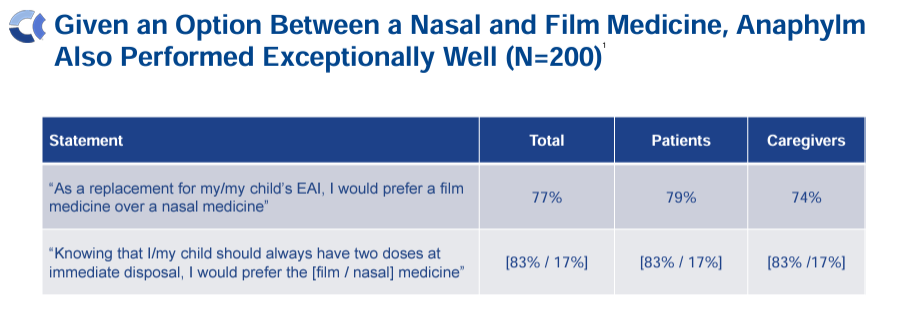

This survey conducted by Aquestive indicates that patients and practitioners would strongly prefer sublingual over nasal administration:

Neffy received a CRL from the FDA in September 2023 which requested that ARS conduct an additional study of Neffy in patients with nasal rhinitis (swelling). This was a surprise to the investment community (with some citing the pervasive influence of “Big Pharma”), but has already been resolved, with ARS Pharma reporting positive results from the trial a few weeks ago and a resubmission expected in the next couple months, which could potentially put the approval of Neffy in the 4Q24. We would view the approval of Neffy as a positive event for Aquestive as it would show the FDA’s willingness to award approvals to next generation epinephrine products.

While Neffy (and perhaps other intranasal products) looks to have about a 1-year head start over Anaphylm which will allow ARS Pharma the advantage of being able to build relationships with physicians, we strongly believe that a sublingual formulation will disproportionately win market share in the long-run.

Market Opportunity

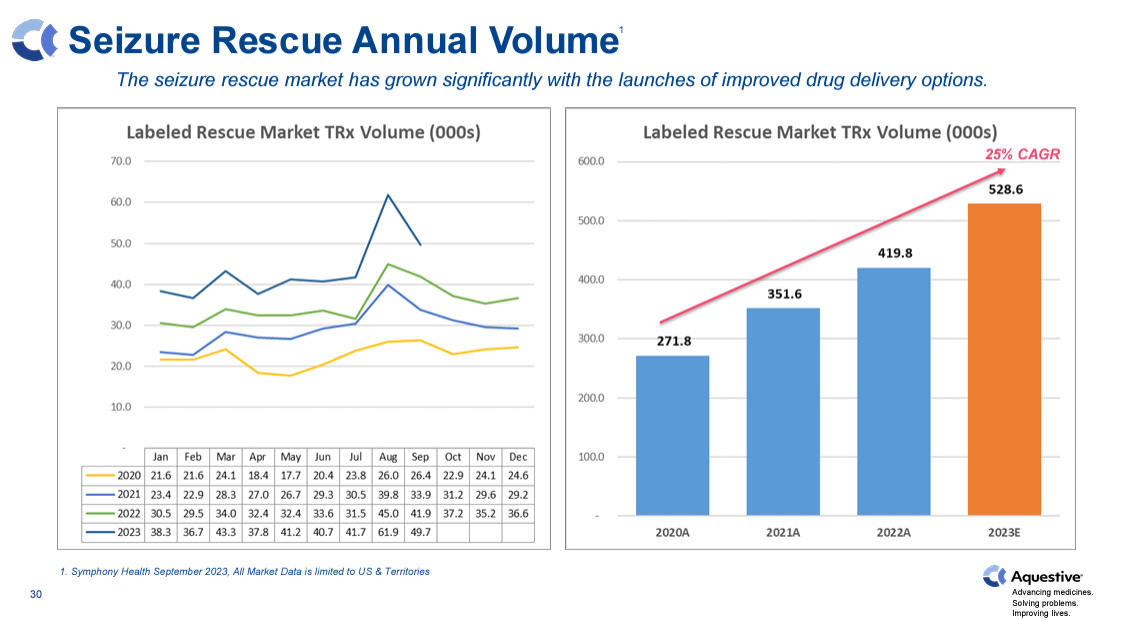

There are an estimated ~30 million people in the US that are at chronic risk of acute allergic reaction or anaphylactic episodes. Despite anaphylaxis being a serious risk, up to 50-60% of patients either don’t fill their prescriptions or do not carry their autoinjector for fear of needles or the hassle of carrying around a bulky autoinjector case.

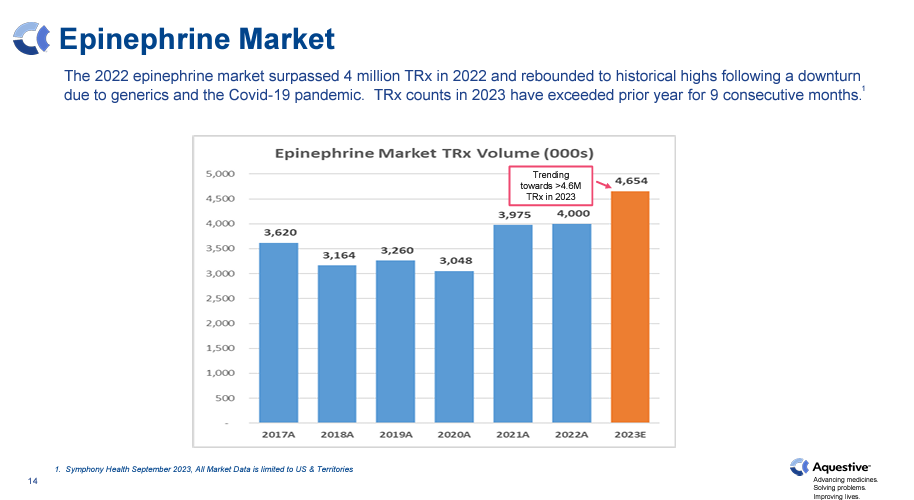

Even with a large portion of patients not filling their prescriptions, there were ~5 million epinephrine prescriptions filled last year, rising steadily each year since the 2020 COVID-19 low.

For context, Mylan’s EpiPen reached over $1.3 billion in annual sales in the 2010’s and the generic epinephrine auto-injector market is estimated at over $1 billion today.

Market Expansion

Anaphylm (and other no-needle options) will likely expand yearly prescriptions significantly, not only because patients prefer a no-needle option, but also because remove the hesitancy of patients to actually use their emergency device in the early stages of an expected reaction, which necessitates a refill prescription.

Even the allergy patients that regularly carry their injectable device often wait until the last possible moment to deploy it or just don’t not use it at all, because of the severity of an intramuscular injection. Patients carrying either Anaphylm (and intranasal products) will be much more willing to deploy their rescue epinephrine in the early stages of a potential reaction.

Where Anaphylm has a distinct advantage from a market expansion perspective over intranasal options like Neffy is that, as a result of its superior form factor and convenience, we believe patients will be much more likely to actually carry their Anaphylm at all times (passively, in their phone case or wallet), while we expect many patients will grow tired of the hassle of remembering to take their Neffy case with them everywhere. Anaphylm is thus more likely to be on-hand during an emergency, leading to higher annual refill prescription rates, all while providing a superior patient experience.

As a result of multiple improvements inherent to no-needle options, ARS Pharma projects that the market for epinephrine prescriptions could nearly triple to 14 million by 2034. Our forecasts are more conservative at 9.8 million prescriptions in 2034 (discussed in Valuation and Revenue Model), though still representing a robust 8% CAGR.

Regardless of sublingual vs. intranasal, the unifying consensus in the allergic reaction space is that patients desperately need a better alternative to auto-injectors. In an ARS Pharma survey, the overwhelming majority of treating physicians said they would prescribe Neffy within one year of approval, demonstrating the market’s eagerness to adopt new treatments:

Libervant and Cluster Seizures

As we mentioned in the intro, Libervant is a unique situation. The FDA has acknowledged Libervant’s safety and efficacy profile by awarding tentative approval in seizure cluster patients aged 12+, though the approval is subject to an Orphan Drug Exclusivity (ODE) block held by Neurelis’s Valtoco (nasal diazepam), which was approved in 2020 in patients aged 6+. The ODE expires in January 2027.

Following the ODE ruling, Aquestive indicated that it would attempt to work with the FDA to circumvent the block by demonstrating Libervant’s superior absorption versus Valtoco following a meal. Aquestive even contracted a third party to run a trial of Valtoco which it says demonstrated a significant decrease (48%) in absorption of Valtoco following a fatty meal. The FDA decided this evidence was not sufficient, however, and the effort to overturn the ODE in children aged 12+ seems to have stalled, with the company no longer actively reporting on it in their earnings calls, though it still appears in the slide deck.

Libervant’s existing tentative approval, along with trial data showing equivalence to rectal diazepam (Diastat; the only approved drug in this age cohort), suggest a high likelihood of FDA approval on the April 28th PDUFA date.

Market Opportunity

There are ~1 million epilepsy patients that suffer from uncontrolled seizure clusters. The market for rescue medicines has grown consistently in recent years, driven by Valtoco and Nayzilam (UCB; nasal version of midazolam) which have provided better alternatives to rectal Diastat.

Libervant’s initial market in children aged 2-5 is small, accounting for around 15% of cluster seizure prescriptions historically. At around 5k prescriptions per month, Libervant would do around $20 million of revenue if it captured the majority of the market (assuming $400 ASP).

Neurelis

In a recent R&D Day, Neurelis mentioned that Valtoco, which is approved in children 12+ and adults, did over $115 million of revenue in 2023, representing 60% y/y growth. In 2021, its first full year of approval, Valtoco did more than $40 million of revenue. Valtoco’s rapid market uptake and continued growth speak to the potential the seizure cluster market, when and if Libervant can expand to other age cohorts.

Conclusion

We will seek to get a better idea of how Libervant, if approved in ages 2-5, could be prescribed off-label to older patients, which could allow it to become a meaningful revenue generator in the near term. Regardless, Libervant has meaningful long-term value potential as it gains label expansion as the only sublingual product for seizure clusters. We assign a very small probability to the potential for Aquestive to parlay approval in age 2-5 into overturning the ODE block in older patients, which would be a surprise upside event.

While clearly overshadowed by Anaphylm, Libervant is an interesting first-out-of-the-gate with a very well defined, if small, unmet need and patient population. We will be interested to see what comes of the ongoing partnership discussions, which could bring attractive terms given the performance of Valtoco.

AQST-108

AQST-108, Aquestive’s topical cream product containing an active ingredient from its Adrenoverse technology (library of epinephrine/adrenergic compounds), has remained somewhat mysterious. On the 4Q23 earnings call, CEO Daniel Barber said that Aquestive is currently testing AQST-108 first-in-human trials aiming to characterize its transdermal absorption profile. The company plans to share more updates on AQST-108 later in 2024.

Epinephrine does not absorb well through the skin, a problem Aquestive believes they have overcome, allowing them to potentially advance AQST-108 in multiple dermatological indications. Epinephrine is well known to inhibit histamine release from mast cells (as in an allergic reaction), and thus we think that potential indication Aquestive may target for AQST-108 would be atopic dermatitis (20+ million US patients), rosacea (16 million US patients), or perhaps even psoriasis (7 million US patients).

We will have to wait for more information throughout 2024, but early proof of concept results in a large indication(s) could present AQST-108 as a major opportunity over the longer-term.

PharmFilm and Adrenaverse

Aquestive appears to have an impressive formulation and absorption technology platform, as evidenced by its PharmFilm technology which has already been utilized via licensing agreements in multiple products (e.g. Indivior’s Suboxone), as well as its status as the only company advancing sublingual formulations in its two lead indications.

In addition to Libervant, we think Aquestive may be able to pursue licensing arrangements to create sublingual formulations of approved drugs in other acute psychiatric/neuro indications such as acute symptoms of schizophrenia or Alzheimer’s disease agitation. For example, Neurelis is pursuing a nasal formulation of olanzapine/Zyprexa for agitation episodes in schizophrenia and bipolar mania.

Additionally, Aquestive’s Adrenaverse platform appears to be validated and could potentially produce additional pipeline programs, though we expect the company to focus on AQST-108 for the time being.

Financial Position

Aquestive recently refinanced its debt in November 2023 into a $45 million note outstanding which carries a 13.5% interest rate. The refinance allowed Aquestive to avoid beginning principal repayments (which are now pushed out to June of 2026). The new loan also comes with tiered royalties of 1-2% of Anaphylm net sales for the first 8 years of availability.

The company had $24 million of cash as of 12/31/23 and has managed its cash relatively well, partially supported by its base business which turned marginally profitable in 2023. In 2023, Aquestive used its ATM to raise $9 million, with $24 million remaining on the facility.

If Aquestive’s stock continues its momentum, it may be prudent for the company to raise $20-50 million in an equity offering, which could allow them to pay off their outstanding debt obligation and provide the balance sheet with additional cushion.

Additionally, the company may soon announce non-dilutive financing via the out-licensing of either Libervant or the ex-US rights to Anaphylm, which would strengthen the balance sheet.

Valuation and Revenue Model

Relative Valuation

Aquestive is trading at $445 million of market cap. Using ARS Pharma ($880 million market cap) as a direct comparison implies a 97% upside. While ARS Pharma’s Neffy is ~1 year ahead of Aquestive, which warrants a premium, we believe Anaphylm will ultimately capture a larger portion of the market. Also, we note that ARS Pharma has three nasal competitors which are expected to submit NDAs in 2024 or 2025, while Anaphylm is highly unique as the only sublingual formulation in development that we are aware of. Given that Aquestive also has other drugs in its pipeline, including a potentially interesting topical dermatology product, while ARS Pharma relies solely on Neffy, we think there is a clear thesis for Aquestive to surpass ARS Pharma’s market cap over the next 12-24 months.

From another angle, Neurelis raised $115 million in March 2021, which appears to have been at a post-money valuation of $454 million, essentially in-line with Aquestive’s current market cap. This accounts for Neurelis’s focus on seizure clusters, which is 5-10% the size of the allergy/anaphylaxis market. Still, we think Neurelis is probably worth substantially more in 2024 as it has demonstrated commercial success and also is beginning to advance a pipeline of nasal formulations of already-approved drug products for other CNS indications. Interestingly, ARS Pharma in-licensed Neurelis’s nasal formulation technology to create Neffy.

Revenue Model

On a fundamental basis, we expect Anaphylm to receive approval in late 2025 and to reach 20% market share of new epinephrine prescriptions by 2027, which at $350 per pack-of-two would yield $442 million of revenue. The customary 3x sales multiple for biopharma would yield a $1.3 billion market cap, implying 198% upside to the current price.

We think our market share curve could be conservative depending on market/physician/patient adoption of sublingual versus nasal. Also, Aquestive may deserve higher than a 3x sales multiple in 2027 given that we expect Anaphylm to have strong growth into the 2030s. At a 5x sales multiple of our 2027 sales estimate, Aquestive would trade at $2.2 billion valuation, representing 394% upside from current levels.

Our model assumes steady overall prescription growth for the epinephrine market to 8 million prescriptions by 2030, representing an 8% CAGR, which we believe are supported by the market expansion dynamics discussed. We also note that our total Rx projections are quite conservative compared to ARS Pharma’s projection of 14 million annual prescriptions by 2034. We project 55%+ market share for Anaphylm in 2033, which could be conservative.

We believe a $350 is a fair, if somewhat conservative, estimate of ASP based on the generic version of EpiPen which appears to sell for $200-600 per two-pack, while Neurelis’s Valtoco appears to sell for $600-700 per two-pack.

Our revenue model excludes Libervant, which is expected to begin contributing to revenue starting late 2024/2025 (and may result in a licensing deal in the near future), and AQST-108, which would likely be in mid-to-late stage trials by 2027.

Even if Anaphylm captures only 30% market share by 2030, the company will be doing ~$1 billion in revenue. Especially as the commercialization of Anaphylm draws nearer, we think the market will begin to more accurately value the magnitude of its opportunity.

Risks

Most of the risks we are focused on relate to potential issues the FDA could find with Anaphylm’s NDA package, causing Aquestive to have to run additional PK/PD characterization trials that run into 2025. For example, the FDA issued a surprise CRL to ARS Pharma for Neffy last year requiring them to run another small study, delaying its expected commercialization by roughly a year. We note that Aquestive has the benefit of factoring these events into their development plan.

High Plasma Concentrations

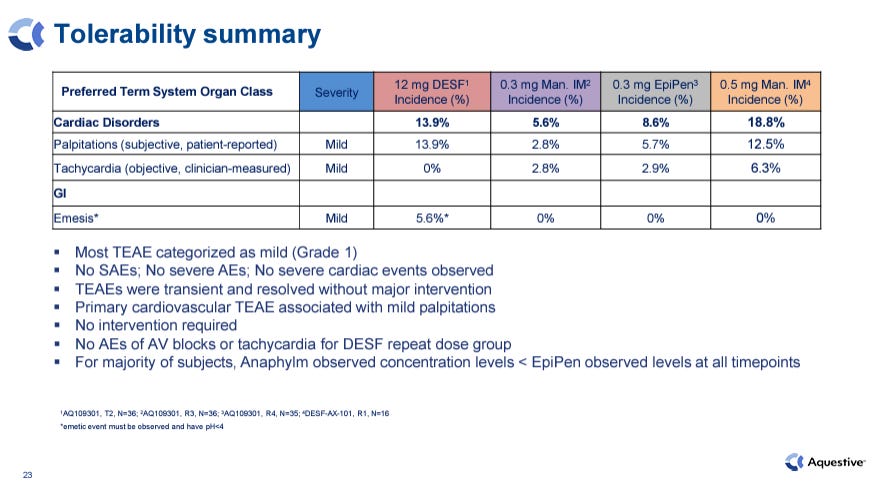

While we believe Anaphylm’s rapid and strong effect is a positive for a rescue indication like allergy and anaphylaxis, it does seem that concentrations of epinephrine in the blood delivered by Anaphylm can reach significantly higher levels than those of EpiPen and other injectable options in some scenarios, namely during repeat dosing context. The FDA has guided that next-gen epinephrine products delivering concentrations above known EpiPen levels must be justified from a safety profile, which we believe is the case for Anaphylm.

Side Effect Profile

Upon repeat dosing in the pivotal Phase 3, Anaphylm’s cardiac side effect profile goes from a very favorable (1%) to about 14% of patients experiencing palpitations. While it is still roughly in-line with repeat doses of injectable forms and Anaphylm looks much safer based on tachycardia (0%), the modestly higher rate of palpitations vs. EpiPen could speak to Anaphylm’s high plasma concentration.

Relatedly, Anaphylm did report vomiting in 3 of its 64-patient pivotal Phase 3 trials. Only 1 of these patients occurred in the 64-patient single dose study, which covers most use cases. The company has stated that it will characterize each of the vomiting cases to the FDA. 1-5% vomiting rate is a very minor concern in this indication in our opinion.

Valtoco ODE

There seems to be some outside speculation of a small chance that the ODE for Valtaco in children aged 6+ could be determined by the Office of Orphan Products Development to apply to children aged 2-5 as well. Aquestive’s understanding, however, is that ODE is specific to the indication and age, meaning Libervant is expected to be marketable right away.

Financial Position

If the company is not able to strike a licensing deal for Libervant or Anaphylm in the next couple of quarters, the company may be forced to commercialize Libervant on its own, which would likely require additional capital.

Conclusion

Powered by its powerful sublingual formulation technology, Aquestive’s Anaphylm is well positioned to disrupt and significantly expand the $1+ billion acute allergic reaction and anaphylaxis market. We believe Anaphylm’s ease of administration and tiny, slender form factor make it a superior product to the nasal spray devices which will ultimately deliver a completely new treatment paradigm for patients where epinephrine rescue treatment is available essentially anytime and anywhere.

While Anaphylm is about 1 year behind its primary nasal competitor Neffy, we believe these advantages will deliver substantial long-term market share and revenue growth for Anaphylm starting shortly after its expected FDA approval in the 2H25. With the added upside potential of a near-term FDA approval and out-licensing deal for Libervant, as well as the AQST-108 topical cream in dermatological indications, Aquestive presents an attractive buy and hold opportunity for years to come.